Truncated Multivariate Student t Density

dtmvt.RdThis function provides the joint density function for the truncated multivariate Student t

distribution with mean vector equal to mean, covariance matrix

sigma, degrees of freedom parameter df and

lower and upper truncation points lower and upper.

Arguments

- x

Vector or matrix of quantiles. If

xis a matrix, each row is taken to be a quantile.- mean

Mean vector, default is

rep(0, nrow(sigma)).- sigma

Covariance matrix, default is

diag(length(mean)).- df

degrees of freedom parameter

- lower

Vector of lower truncation points, default is

rep(-Inf, length = length(mean)).- upper

Vector of upper truncation points, default is

rep( Inf, length = length(mean)).- log

Logical; if

TRUE, densities d are given as log(d).

Details

The Truncated Multivariate Student t Distribution is a conditional Multivariate Student t distribution subject to (linear) constraints \(a \le \bold{x} \le b\).

The density of the \(p\)-variate Multivariate Student t distribution with \(\nu\) degrees of freedom is $$ f(\bold{x}) = \frac{\Gamma((\nu + p)/2)}{(\pi\nu)^{p/2} \Gamma(\nu/2) \|\Sigma\|^{1/2}} [ 1 + \frac{1}{\nu} (x - \mu)^T \Sigma^{-1} (x - \mu) ]^{- (\nu + p) / 2} $$ The density of the truncated distribution \(f_{a,b}(x)\) with constraints \((a \le x \le b)\) is accordingly $$ f_{a,b}(x) = \frac{f(\bold{x})} {P(a \le x \le b)} $$

Value

a numeric vector with density values

See also

References

Geweke, J. F. (1991) Efficient simulation from the multivariate normal and Student-t distributions subject to linear constraints and the evaluation of constraint probabilities. https://www.researchgate.net/publication/2335219_Efficient_Simulation_from_the_Multivariate_Normal_and_Student-t_Distributions_Subject_to_Linear_Constraints_and_the_Evaluation_of_Constraint_Probabilities

Samuel Kotz, Saralees Nadarajah (2004). Multivariate t Distributions and Their Applications. Cambridge University Press

Examples

# Example

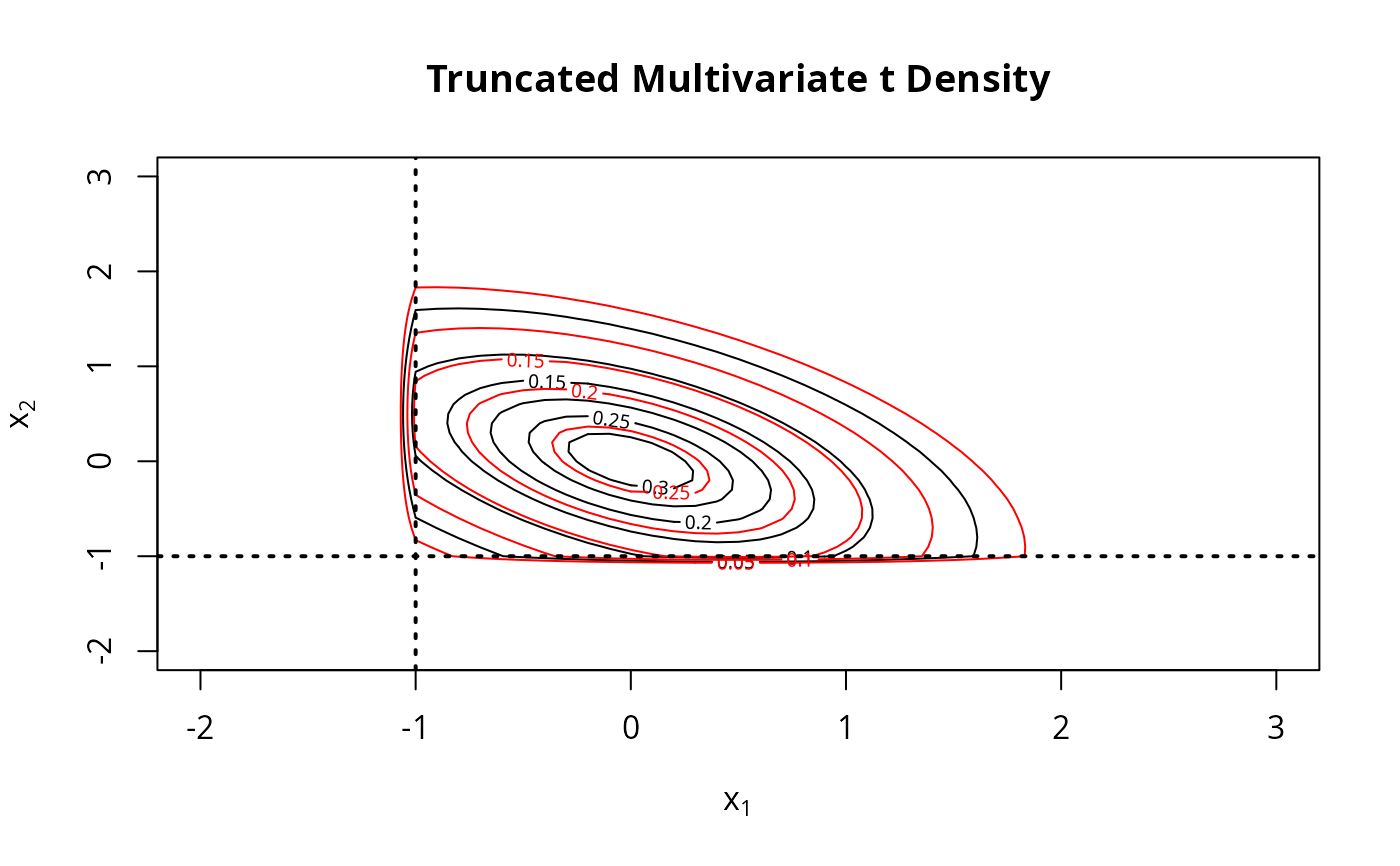

x1 <- seq(-2, 3, by=0.1)

x2 <- seq(-2, 3, by=0.1)

mean <- c(0,0)

sigma <- matrix(c(1, -0.5, -0.5, 1), 2, 2)

lower <- c(-1,-1)

density <- function(x)

{

z=dtmvt(x, mean=mean, sigma=sigma, lower=lower)

z

}

fgrid <- function(x, y, f)

{

z <- matrix(nrow=length(x), ncol=length(y))

for(m in 1:length(x)){

for(n in 1:length(y)){

z[m,n] <- f(c(x[m], y[n]))

}

}

z

}

# compute multivariate-t density d for grid

d <- fgrid(x1, x2, function(x) dtmvt(x, mean=mean, sigma=sigma, lower=lower))

# compute multivariate normal density d for grid

d2 <- fgrid(x1, x2, function(x) dtmvnorm(x, mean=mean, sigma=sigma, lower=lower))

# plot density as contourplot

contour(x1, x2, d, nlevels=5, main="Truncated Multivariate t Density",

xlab=expression(x[1]), ylab=expression(x[2]))

contour(x1, x2, d2, nlevels=5, add=TRUE, col="red")

abline(v=-1, lty=3, lwd=2)

abline(h=-1, lty=3, lwd=2)