Glance accepts a model object and returns a tibble::tibble()

with exactly one row of model summaries. The summaries are typically

goodness of fit measures, p-values for hypothesis tests on residuals,

or model convergence information.

Glance never returns information from the original call to the modeling function. This includes the name of the modeling function or any arguments passed to the modeling function.

Glance does not calculate summary measures. Rather, it farms out these

computations to appropriate methods and gathers the results together.

Sometimes a goodness of fit measure will be undefined. In these cases

the measure will be reported as NA.

Glance returns the same number of columns regardless of whether the

model matrix is rank-deficient or not. If so, entries in columns

that no longer have a well-defined value are filled in with an NA

of the appropriate type.

# S3 method for class 'gmm'

glance(x, ...)Arguments

- x

A

gmmobject returned fromgmm::gmm().- ...

Additional arguments. Not used. Needed to match generic signature only. Cautionary note: Misspelled arguments will be absorbed in

..., where they will be ignored. If the misspelled argument has a default value, the default value will be used. For example, if you passconf.lvel = 0.9, all computation will proceed usingconf.level = 0.95. Two exceptions here are:

See also

Other gmm tidiers:

tidy.gmm()

Value

A tibble::tibble() with exactly one row and columns:

- df

Degrees of freedom used by the model.

- df.residual

Residual degrees of freedom.

- nobs

Number of observations used.

- p.value

P-value corresponding to the test statistic.

- statistic

Test statistic.

Examples

# load libraries for models and data

library(gmm)

# examples come from the "gmm" package

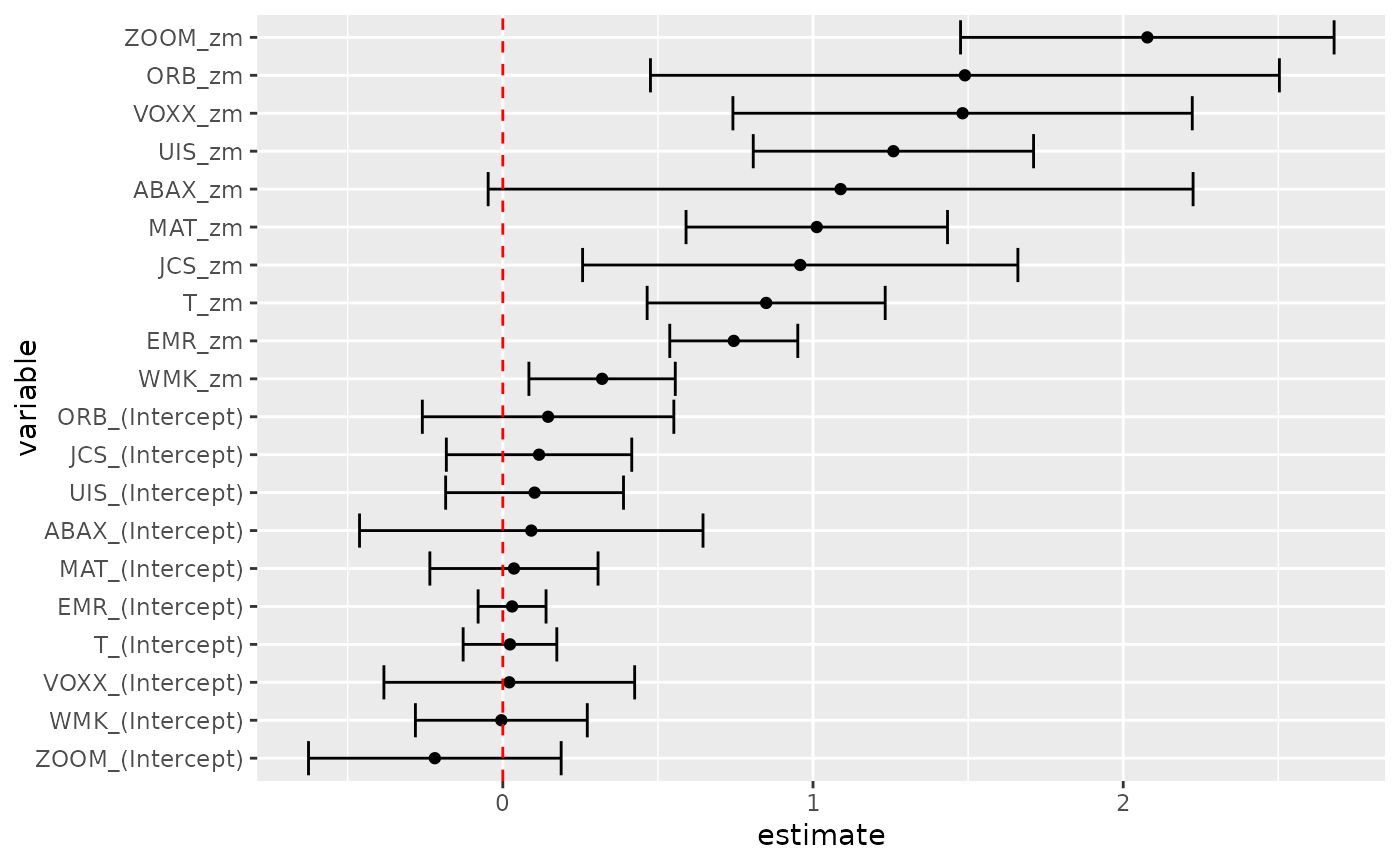

# CAPM test with GMM

data(Finance)

r <- Finance[1:300, 1:10]

rm <- Finance[1:300, "rm"]

rf <- Finance[1:300, "rf"]

z <- as.matrix(r - rf)

t <- nrow(z)

zm <- rm - rf

h <- matrix(zm, t, 1)

res <- gmm(z ~ zm, x = h)

# tidy result

tidy(res)

#> # A tibble: 20 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11

tidy(res, conf.int = TRUE)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1 -0.282 0.272

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1 -0.184 0.389

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1 -0.259 0.551

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1 -0.235 0.307

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1 -0.462 0.645

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1 -0.128 0.174

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1 -0.0796 0.139

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1 -0.182 0.416

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1 -0.383 0.425

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1 -0.626 0.188

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3 0.0841 0.556

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8 0.807 1.71

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3 0.476 2.50

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6 0.591 1.43

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2 -0.0472 2.23

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5 0.465 1.23

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12 0.538 0.951

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3 0.257 1.66

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5 0.742 2.22

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11 1.48 2.68

tidy(res, conf.int = TRUE, conf.level = .99)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1 -0.369 0.359

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1 -0.274 0.479

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1 -0.387 0.679

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1 -0.320 0.392

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1 -0.636 0.819

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1 -0.175 0.222

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1 -0.114 0.174

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1 -0.276 0.510

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1 -0.510 0.552

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1 -0.754 0.316

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3 0.0100 0.630

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8 0.665 1.85

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3 0.157 2.82

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6 0.458 1.57

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2 -0.404 2.58

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5 0.345 1.35

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12 0.473 1.02

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3 0.0367 1.88

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5 0.509 2.46

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11 1.29 2.87

# coefficient plot

library(ggplot2)

library(dplyr)

tidy(res, conf.int = TRUE) %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

#> Warning: model order: 1 singularities in the computation of the projection matrix results are only valid up to model order 0

#> Error in AA %*% t(X) : requires numeric/complex matrix/vector arguments

#> Error in AllArg$bw(obj, order.by = AllArg$order.by, kernel = AllArg$kernel, prewhite = AllArg$prewhite, ar.method = AllArg$ar.method, approx = AllArg$approx): VAR(1) prewhitening of estimating functions failed

tidy(res_black)

#> Error: object 'res_black' not found

tidy(res_black, conf.int = TRUE)

#> Error: object 'res_black' not found

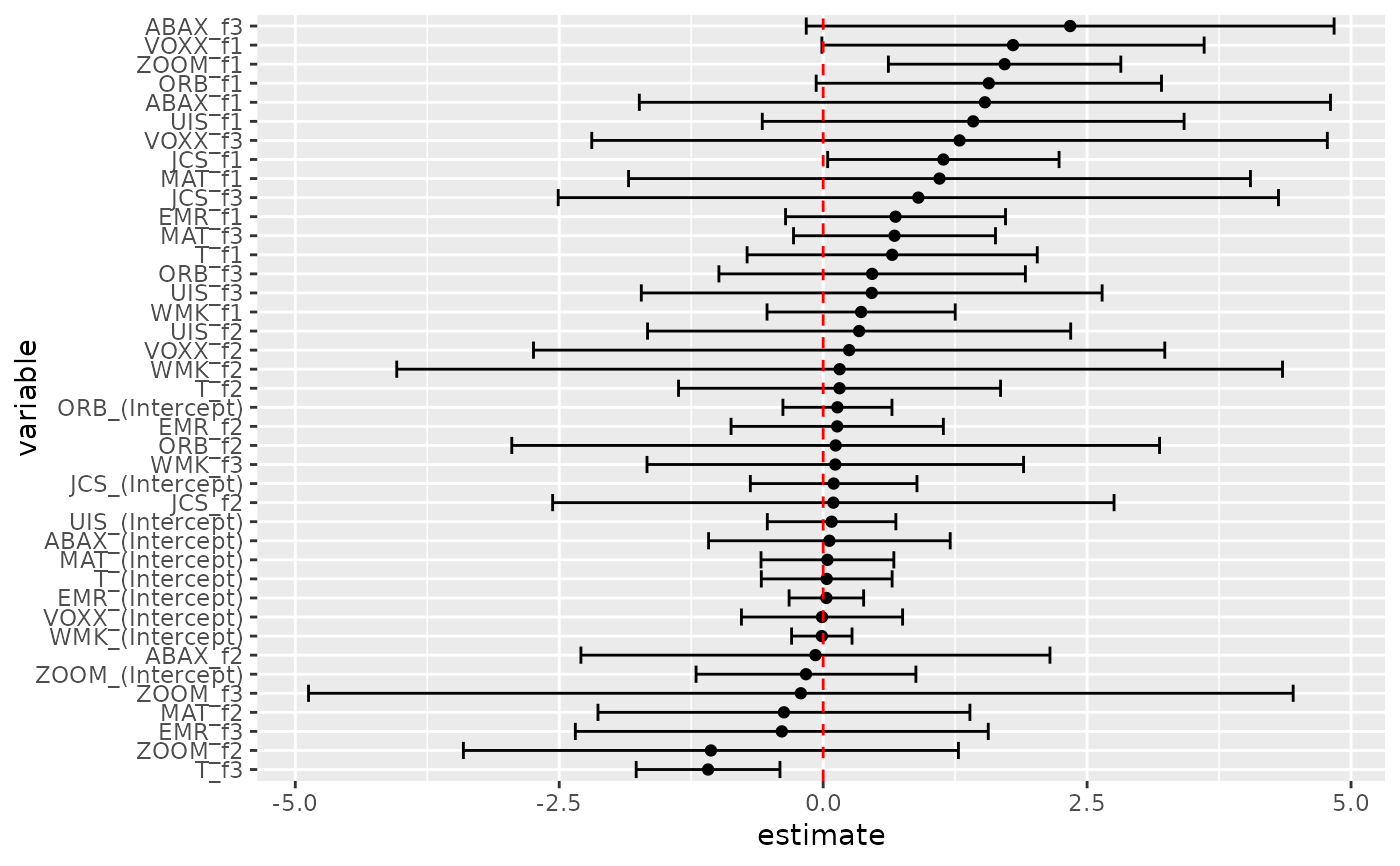

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.0127 0.146 -0.0873 0.930 -0.299 0.273

#> 2 UIS_(Intercept) 0.0799 0.311 0.257 0.797 -0.529 0.689

#> 3 ORB_(Intercept) 0.135 0.263 0.514 0.608 -0.381 0.652

#> 4 MAT_(Intercept) 0.0405 0.321 0.126 0.900 -0.589 0.670

#> 5 ABAX_(Intercept) 0.0589 0.584 0.101 0.920 -1.09 1.20

#> 6 T_(Intercept) 0.0337 0.316 0.107 0.915 -0.586 0.653

#> 7 EMR_(Intercept) 0.0304 0.180 0.169 0.866 -0.323 0.383

#> 8 JCS_(Intercept) 0.0994 0.403 0.247 0.805 -0.690 0.889

#> 9 VOXX_(Intercept) -0.0108 0.389 -0.0279 0.978 -0.774 0.752

#> 10 ZOOM_(Intercept) -0.163 0.531 -0.306 0.759 -1.20 0.878

#> # ℹ 30 more rows

# coefficient plot

td2 %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

#> Warning: model order: 1 singularities in the computation of the projection matrix results are only valid up to model order 0

#> Error in AA %*% t(X) : requires numeric/complex matrix/vector arguments

#> Error in AllArg$bw(obj, order.by = AllArg$order.by, kernel = AllArg$kernel, prewhite = AllArg$prewhite, ar.method = AllArg$ar.method, approx = AllArg$approx): VAR(1) prewhitening of estimating functions failed

tidy(res_black)

#> Error: object 'res_black' not found

tidy(res_black, conf.int = TRUE)

#> Error: object 'res_black' not found

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.0127 0.146 -0.0873 0.930 -0.299 0.273

#> 2 UIS_(Intercept) 0.0799 0.311 0.257 0.797 -0.529 0.689

#> 3 ORB_(Intercept) 0.135 0.263 0.514 0.608 -0.381 0.652

#> 4 MAT_(Intercept) 0.0405 0.321 0.126 0.900 -0.589 0.670

#> 5 ABAX_(Intercept) 0.0589 0.584 0.101 0.920 -1.09 1.20

#> 6 T_(Intercept) 0.0337 0.316 0.107 0.915 -0.586 0.653

#> 7 EMR_(Intercept) 0.0304 0.180 0.169 0.866 -0.323 0.383

#> 8 JCS_(Intercept) 0.0994 0.403 0.247 0.805 -0.690 0.889

#> 9 VOXX_(Intercept) -0.0108 0.389 -0.0279 0.978 -0.774 0.752

#> 10 ZOOM_(Intercept) -0.163 0.531 -0.306 0.759 -1.20 0.878

#> # ℹ 30 more rows

# coefficient plot

td2 %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)