Tidy summarizes information about the components of a model. A model component might be a single term in a regression, a single hypothesis, a cluster, or a class. Exactly what tidy considers to be a model component varies across models but is usually self-evident. If a model has several distinct types of components, you will need to specify which components to return.

# S3 method for class 'gmm'

tidy(x, conf.int = FALSE, conf.level = 0.95, exponentiate = FALSE, ...)Arguments

- x

A

gmmobject returned fromgmm::gmm().- conf.int

Logical indicating whether or not to include a confidence interval in the tidied output. Defaults to

FALSE.- conf.level

The confidence level to use for the confidence interval if

conf.int = TRUE. Must be strictly greater than 0 and less than 1. Defaults to 0.95, which corresponds to a 95 percent confidence interval.- exponentiate

Logical indicating whether or not to exponentiate the the coefficient estimates. This is typical for logistic and multinomial regressions, but a bad idea if there is no log or logit link. Defaults to

FALSE.- ...

Additional arguments. Not used. Needed to match generic signature only. Cautionary note: Misspelled arguments will be absorbed in

..., where they will be ignored. If the misspelled argument has a default value, the default value will be used. For example, if you passconf.lvel = 0.9, all computation will proceed usingconf.level = 0.95. Two exceptions here are:

See also

Other gmm tidiers:

glance.gmm()

Value

A tibble::tibble() with columns:

- conf.high

Upper bound on the confidence interval for the estimate.

- conf.low

Lower bound on the confidence interval for the estimate.

- estimate

The estimated value of the regression term.

- p.value

The two-sided p-value associated with the observed statistic.

- statistic

The value of a T-statistic to use in a hypothesis that the regression term is non-zero.

- std.error

The standard error of the regression term.

- term

The name of the regression term.

Examples

# load libraries for models and data

library(gmm)

# examples come from the "gmm" package

# CAPM test with GMM

data(Finance)

r <- Finance[1:300, 1:10]

rm <- Finance[1:300, "rm"]

rf <- Finance[1:300, "rf"]

z <- as.matrix(r - rf)

t <- nrow(z)

zm <- rm - rf

h <- matrix(zm, t, 1)

res <- gmm(z ~ zm, x = h)

# tidy result

tidy(res)

#> # A tibble: 20 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11

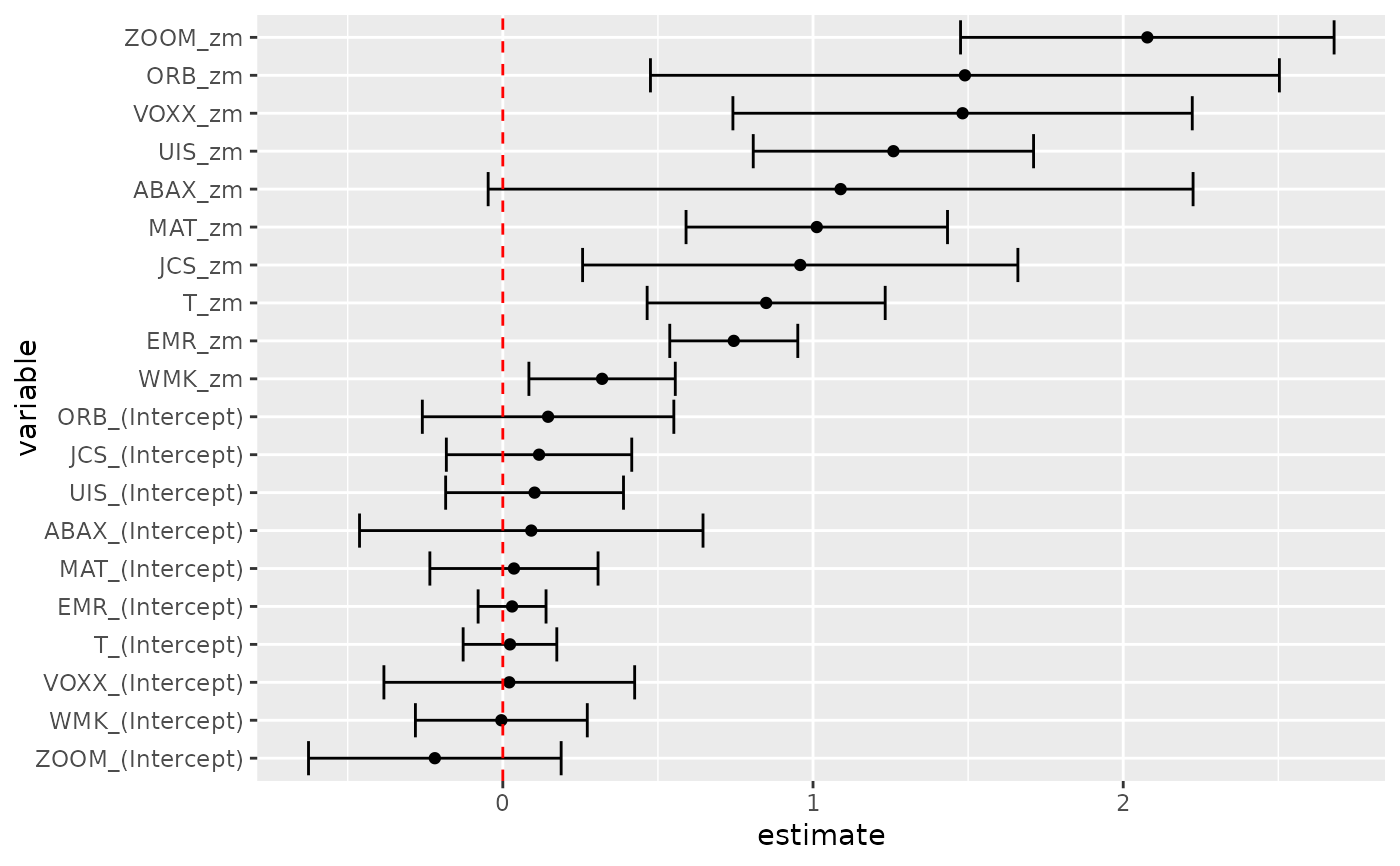

tidy(res, conf.int = TRUE)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1 -0.282 0.272

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1 -0.184 0.389

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1 -0.259 0.551

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1 -0.235 0.307

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1 -0.462 0.645

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1 -0.128 0.174

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1 -0.0796 0.139

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1 -0.182 0.416

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1 -0.383 0.425

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1 -0.626 0.188

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3 0.0841 0.556

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8 0.807 1.71

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3 0.476 2.50

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6 0.591 1.43

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2 -0.0472 2.23

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5 0.465 1.23

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12 0.538 0.951

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3 0.257 1.66

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5 0.742 2.22

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11 1.48 2.68

tidy(res, conf.int = TRUE, conf.level = .99)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00471 0.141 -0.0333 9.73e- 1 -0.369 0.359

#> 2 UIS_(Intercept) 0.102 0.146 0.700 4.84e- 1 -0.274 0.479

#> 3 ORB_(Intercept) 0.146 0.207 0.706 4.80e- 1 -0.387 0.679

#> 4 MAT_(Intercept) 0.0359 0.138 0.260 7.95e- 1 -0.320 0.392

#> 5 ABAX_(Intercept) 0.0917 0.282 0.325 7.45e- 1 -0.636 0.819

#> 6 T_(Intercept) 0.0231 0.0770 0.300 7.64e- 1 -0.175 0.222

#> 7 EMR_(Intercept) 0.0299 0.0559 0.535 5.93e- 1 -0.114 0.174

#> 8 JCS_(Intercept) 0.117 0.152 0.766 4.44e- 1 -0.276 0.510

#> 9 VOXX_(Intercept) 0.0209 0.206 0.101 9.19e- 1 -0.510 0.552

#> 10 ZOOM_(Intercept) -0.219 0.208 -1.05 2.92e- 1 -0.754 0.316

#> 11 WMK_zm 0.320 0.120 2.66 7.84e- 3 0.0100 0.630

#> 12 UIS_zm 1.26 0.231 5.46 4.72e- 8 0.665 1.85

#> 13 ORB_zm 1.49 0.517 2.88 3.97e- 3 0.157 2.82

#> 14 MAT_zm 1.01 0.215 4.71 2.51e- 6 0.458 1.57

#> 15 ABAX_zm 1.09 0.580 1.88 6.03e- 2 -0.404 2.58

#> 16 T_zm 0.849 0.196 4.34 1.45e- 5 0.345 1.35

#> 17 EMR_zm 0.745 0.105 7.07 1.53e-12 0.473 1.02

#> 18 JCS_zm 0.959 0.358 2.68 7.40e- 3 0.0367 1.88

#> 19 VOXX_zm 1.48 0.378 3.92 8.73e- 5 0.509 2.46

#> 20 ZOOM_zm 2.08 0.307 6.76 1.35e-11 1.29 2.87

# coefficient plot

library(ggplot2)

library(dplyr)

tidy(res, conf.int = TRUE) %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

#> Warning: model order: 1 singularities in the computation of the projection matrix results are only valid up to model order 0

#> Error in AA %*% t(X) : requires numeric/complex matrix/vector arguments

#> Error in AllArg$bw(obj, order.by = AllArg$order.by, kernel = AllArg$kernel, prewhite = AllArg$prewhite, ar.method = AllArg$ar.method, approx = AllArg$approx): VAR(1) prewhitening of estimating functions failed

tidy(res_black)

#> Error: object 'res_black' not found

tidy(res_black, conf.int = TRUE)

#> Error: object 'res_black' not found

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.0127 0.146 -0.0873 0.930 -0.299 0.273

#> 2 UIS_(Intercept) 0.0799 0.311 0.257 0.797 -0.529 0.689

#> 3 ORB_(Intercept) 0.135 0.263 0.514 0.608 -0.381 0.652

#> 4 MAT_(Intercept) 0.0405 0.321 0.126 0.900 -0.589 0.670

#> 5 ABAX_(Intercept) 0.0589 0.584 0.101 0.920 -1.09 1.20

#> 6 T_(Intercept) 0.0337 0.316 0.107 0.915 -0.586 0.653

#> 7 EMR_(Intercept) 0.0304 0.180 0.169 0.866 -0.323 0.383

#> 8 JCS_(Intercept) 0.0994 0.403 0.247 0.805 -0.690 0.889

#> 9 VOXX_(Intercept) -0.0108 0.389 -0.0279 0.978 -0.774 0.752

#> 10 ZOOM_(Intercept) -0.163 0.531 -0.306 0.759 -1.20 0.878

#> # ℹ 30 more rows

# coefficient plot

td2 %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

#> Warning: model order: 1 singularities in the computation of the projection matrix results are only valid up to model order 0

#> Error in AA %*% t(X) : requires numeric/complex matrix/vector arguments

#> Error in AllArg$bw(obj, order.by = AllArg$order.by, kernel = AllArg$kernel, prewhite = AllArg$prewhite, ar.method = AllArg$ar.method, approx = AllArg$approx): VAR(1) prewhitening of estimating functions failed

tidy(res_black)

#> Error: object 'res_black' not found

tidy(res_black, conf.int = TRUE)

#> Error: object 'res_black' not found

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.0127 0.146 -0.0873 0.930 -0.299 0.273

#> 2 UIS_(Intercept) 0.0799 0.311 0.257 0.797 -0.529 0.689

#> 3 ORB_(Intercept) 0.135 0.263 0.514 0.608 -0.381 0.652

#> 4 MAT_(Intercept) 0.0405 0.321 0.126 0.900 -0.589 0.670

#> 5 ABAX_(Intercept) 0.0589 0.584 0.101 0.920 -1.09 1.20

#> 6 T_(Intercept) 0.0337 0.316 0.107 0.915 -0.586 0.653

#> 7 EMR_(Intercept) 0.0304 0.180 0.169 0.866 -0.323 0.383

#> 8 JCS_(Intercept) 0.0994 0.403 0.247 0.805 -0.690 0.889

#> 9 VOXX_(Intercept) -0.0108 0.389 -0.0279 0.978 -0.774 0.752

#> 10 ZOOM_(Intercept) -0.163 0.531 -0.306 0.759 -1.20 0.878

#> # ℹ 30 more rows

# coefficient plot

td2 %>%

mutate(variable = reorder(term, estimate)) %>%

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)